Innovation is a funny thing. It’s rarely about the flashiest idea in the moment — more often, it’s the simple shifts that quietly rewire how industries work. What looks small today can reshape customer behavior, business models, and even entire markets for decades.

That’s why I put together this list of Strategic Innovations that I think had the greatest impact on loyalty as we see it today. Not as a definitive history, but as a perspective on the moments where experimentation sparked transformation. From stamps and co-ops to frequent flyer miles and mobile apps, these programs remind us that the real impact of innovation isn’t always immediate. It’s measured in how long the ripples last.

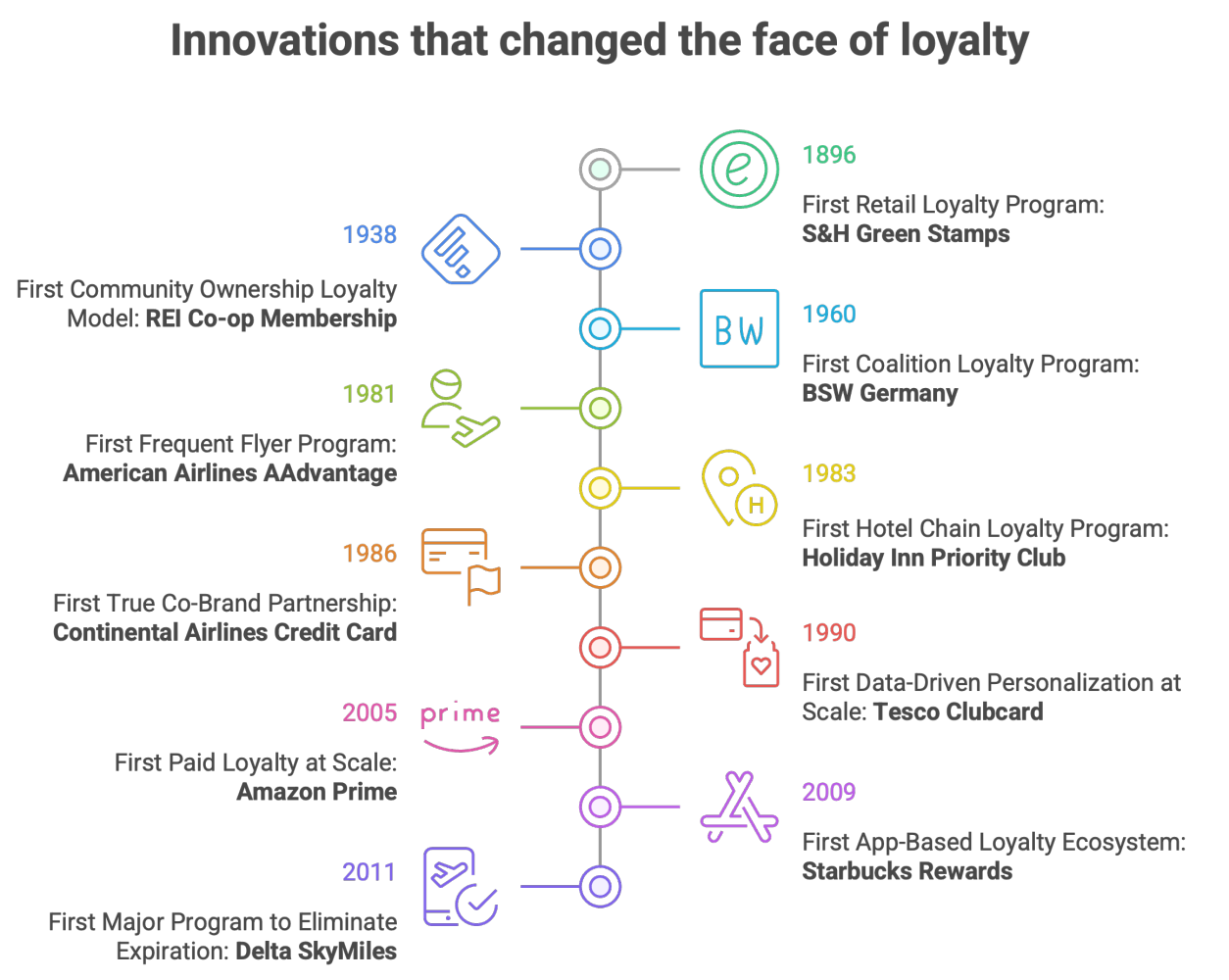

My list (I expect some debate!)

This is my take — informed by experience, but still just one view. I’d love to hear yours. Feel free to reuse the graphic. What would you add? What do you see as the next “first” waiting to happen in our industry?

- American Airlines – The First Frequent Flyer Program (1981)

- Continental Airlines – The First True Co-Branded Credit Card (1986)

- Tesco Clubcard – The First Data-Driven Personalization at Scale (1990s)

- Delta SkyMiles – The First Major Program to Eliminate Expiration (2011)

- REI Co-op Membership – The First Community Ownership Model (1938)

- Amazon Prime – The First Paid Loyalty at Scale (2005)

- Starbucks Rewards – The First App-Based Loyalty Ecosystem (2009)

- BSW Germany – The First Coalition Loyalty Program (1960)

- Holiday Inn Priority Club – The First Hotel Chain Loyalty Program (1983)

- S&H Green Stamps – The First Retail Loyalty Program (1896)

Perspective: Chronological view of strategic innovations

The First Frequent Flyer Program (1981): American Airlines

When American Airlines launched AAdvantage in 1981, it looked like a promotion about free flights. In reality, it was a revolution in customer ownership. Until then, travel agents dominated the booking process, controlling both the transaction and the data. Airlines had no real visibility into who their best customers were, or how often they flew.

AAdvantage changed that forever. By building a membership-based program, American created one of the first large-scale customer databases in commercial aviation. They suddenly had names, addresses, preferences, and behavior patterns. For the first time, an airline could segment, market, and build relationships directly with its passengers.

The program not only transformed airline economics — it also set the standard for modern loyalty: data as a strategic asset. Today’s obsession with first-party data ownership can trace its roots back to that single innovation.

The First True Co-Branded Credit Card (1986): Continental Airlines

The launch of the Continental TravelBank Gold MasterCard was one of the boldest moves in loyalty history. Before this, airline credit cards existed, but they were simply payment methods for flights. Continental, in partnership with Bank of Marine Midland, created something new: everyday spend outside of flying could now earn airline miles.

This changed everything. For consumers, it unlocked loyalty as part of daily life, not just when traveling. For airlines, it opened an entirely new revenue stream that quickly became a financial backbone of the industry. Co-branded credit cards now contribute billions in revenue annually and represent one of the most profitable extensions of loyalty economics anywhere in the world.

Continental didn’t just create a new perk. They redefined the business model of loyalty, proving that the real money wasn’t in the free flight — it was in becoming part of how customers spent every day.

The First Data-Driven Personalization at Scale (1990s): Tesco Clubcard

Tesco’s Clubcard wasn’t just a loyalty card — it was a data engine. With the help of Dunnhumby analytics, Tesco turned transactions into insights. They didn’t just reward purchases; they analyzed them, learned from them, and then reshaped the business accordingly.

The result was personalization on a scale retail had never seen before. Promotions weren’t one-size-fits-all; they were individualized, based on customer shopping habits. But it didn’t stop at marketing. Clubcard data informed pricing, category management, store layouts, and even product development.

The lesson? Loyalty programs aren’t just about rewarding behavior — they can change the behavior of the business itself. Tesco proved that loyalty data is enterprise intelligence, and retailers worldwide have been chasing that model ever since.

The First Major Program to Eliminate Expiration (2011): Delta SkyMiles

It hardly seems like an innovation to eliminate an restriction that was imposed late into the loyalty game. However, when Delta announced that SkyMiles would never expire, it felt like a gift to customers. In an industry where points often vanished if accounts went inactive, Delta’s move stood out as a symbol of trust. It said, your loyalty lasts forever.

But make no mistake — this wasn’t reckless generosity. Delta managed liability through other levers: dynamic award pricing, evolving qualification thresholds, and rules around account activity. By doing so, they set a new industry standard: you can earn goodwill and loyalty without losing control of the balance sheet.

Delta’s move reminds us that sometimes the boldest loyalty innovations aren’t about adding more perks but about removing friction that undermines trust. To the strategists, it was a bold statement about just how much control and predictability their team of analysts had over liability expense and deferred revenue.

The First Community Ownership Model (1938): REI Co-op Membership

Long before loyalty was about points and perks, REI made it about belonging. With a one-time fee, customers became members of the co-op — part-owners of the business. They received annual dividends, voting rights, and exclusive access to gear and events.

The genius of REI’s model was that it built loyalty on identity. Members weren’t just customers; they were part of a community with shared values. Campaigns like “Opt Outside” reinforced that REI wasn’t just a retailer, it was a movement.

REI shows us that the most powerful form of loyalty isn’t transactional — it’s emotional. It’s about making customers feel that they are the brand.

The First Paid Loyalty at Scale (2005): Amazon Prime

Asking customers to pay for loyalty was counterintuitive. Yet Amazon proved the opposite with Prime. For a flat annual fee, members received free two-day shipping. Later, content, music, groceries, and more.

The brilliance of Prime is the flywheel effect. Once a customer becomes a paying member, they use Amazon more frequently to justify the fee, which in turn makes them more loyal. Prime members spend far more than non-members, and their emotional attachment to Amazon skyrocketed.

Prime reframed loyalty economics by proving customers will pay to be loyal if the value is undeniable. It’s not a cost center — it’s a growth engine.

The First App-Based Loyalty Ecosystem (2009): Starbucks Rewards

Starbucks did more than digitize a punch card. By embedding loyalty into its mobile app, Starbucks created an ecosystem that blended payments, ordering, and rewards into one seamless experience.

This wasn’t just about coffee — it was about convenience, data, and engagement. Customers ordered ahead, earned Stars, tracked their progress, and paid with a single tap. Starbucks became one of the first brands to merge commerce and loyalty so tightly that one couldn’t exist without the other.

Starbucks Rewards now accounts for a massive share of U.S. sales. It showed the world that loyalty programs could double as platforms — integrating transactions, data, and engagement into a single customer journey.

The First Coalition Loyalty Program (1960): BSW Germany

While Air Miles popularized coalition loyalty in North America, the German firm BSW (Benefita Shopping Association) pioneered it decades earlier. By uniting multiple merchants under a shared loyalty scheme, BSW allowed customers to earn across categories and redeem in one common pool.

This was the first true ecosystem loyalty model. Instead of one brand carrying the entire weight of the program, many brands shared the cost and benefit of a unified currency. Coalitions taught the world that loyalty could scale faster and stickier when brands joined forces. Today, we see echoes of BSW in ecosystems across retail, travel, and even digital platforms.

The First Hotel Chain Loyalty Program (1983): Holiday Inn Priority Club

Hotels were once local experiences; loyalty was property-by-property. Holiday Inn’s Priority Club changed that by creating a chain-wide recognition and rewards system. This was not as simple as it might seem today as unifying point of sales technologies didn’t exist. Despite these challenges, the program successfully allowed travelers to earn and redeem across the entire network, making loyalty portable.

This simple shift gave global hotel chains a competitive edge. It created status tiers, consistent benefits, and recognition that followed the traveler worldwide. Priority Club became the template for the modern hotel loyalty program, paving the way for giants like Marriott Bonvoy and Hilton Honors.

It’s a reminder that sometimes the most powerful innovations are about consistency at scale.

The First Retail Loyalty Program (1896): S&H Green Stamps

S&H Green Stamps were the cultural grandfather of loyalty. Customers received stamps with purchases, filled booklets, and redeemed them for products in catalogues or redemption centers. The brilliance was in its simplicity: deferred gratification. Customers shifted spend toward stores that offered stamps, because they knew the stamps added up to something tangible.

While the program eventually faded, its DNA lives on in every points-based system today. It proved the universal appeal of earn now, redeem later

The need for more innovation

Innovation doesn’t always announce itself with fireworks. Sometimes it’s a simple shift — a stamp, a database, a dividend — that rewrites the rules for decades. The lesson for our industry is clear: loyalty advances when professionals are willing to experiment, to test bold ideas, and to challenge what feels “normal.” The invitation now is for all of us to keep pushing, to try, to fail, and to build. The next great first will come from those willing to think big and act with courage.